The world debt situation is picking up in the financial press again lately, led by the BIS report published in January 2015 which talks of the enormous 9 Trillion US$ carry trade which we covered here.

Then this was followed by the MCKinsey & Company report published in February, which covered the explosion in debt worldwide since the end of 2007. We covered that here.

So rather than re-publishing the many articles of our present situation, I thought we would re-publish an article our Man. Dir. published in 2013 coming at it from a slightly different angle.

Please note: Disclaimer at the end of this article.

It’s the Debt, Stupid ! (A play on Clinton’s phrase)

BIS complete Policy Reversal

Effect on Precious Metals

Part 1.

Originally published in August 2013 by D Mitchell, Updated March 2015

Clinton’s famous successful 1992 presidential campaign phrase was “It’s the economy, stupid” against sitting president George Bush Senior.

Now that phrase could well be “It’s actually the debt, stupid”.

An economy cannot sustain a future of positive economic growth patterns and employment opportunities for the newer generations if the economy is saddled with debt or to be slightly more explicit “totally insolvent”. The debt servicing makes any growth patterns or a normalization of the economy (contrasting radically to the previous 30 to 40 years) basically impossible.

Speaking to many individuals over the last few years as I have done, they really do not appreciate the situation we find ourselves in looking at the bigger picture and taking into consideration historical precedents. When asked what caused the crisis of 2008'09 they always state the housing crisis of the USA (CDS’s, MBS etc..). That is not strictly true! The housing crisis was only a symptom of the disease and simply the first domino to fall; the disease itself is our Debt Insolvency and that is ongoing and expanding!

Have you ever wondered why this crisis simply has not dissipated, 7 years from when it exploded in our faces in 2008? This was never a liquidity problem (per se) or a productivity issue; it was always a solvency and collateral issue.

China's total debt has quadrupled since 2007, rising to $28 trillion from just $7 trillion before the crisis. At 282pc, China’s debt as a share of economic output is now larger than the United States, and is only surpassed by Japan.

With the global indebtedness reaching its highest level in over 200 years, the IMF has warned the world will need a wave of defaults, savings taxes and higher inflation to finally clear the way for recovery.

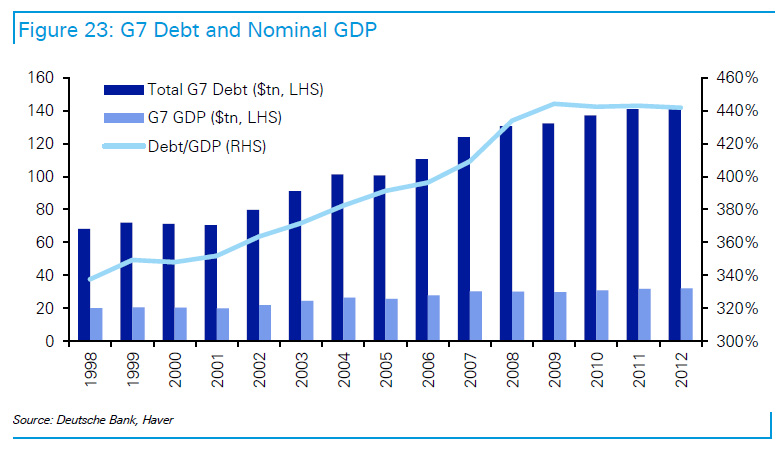

Look at the percentages on the right side of the chart below, these are historical records. This debt simply cannot be carried with higher interest rates – period.

Now this chart below only shows up to 2012 (I originally wrote this article in mid 2013) - However since then debt has risen quite substantially

The fantastic “Great Credit Expansion Cycle” that started around 1951 a few years after the 2nd World War and commenced it’s parabolic rise after 1971 when the USA reneged upon it’s Gold backed currency debt obligations to the World. The scene was set for a massive expansion of credit throughout the world and an unlimited expansion of FIAT Currency ( currency in our present 42 year old Monetary System is actually debt ).

There is always an eventual natural cap on this credit velocity expansion (due to debt servicing requirements – see the flat line since 2009 on chart above) and the immediate effects of this is a natural de-leveraging event with a reduction in debt loads using a combination of outright defaults, debt reduction (mixed with a sprinkling of inflation) until we reach an equilibrium that is sustainable mathematically speaking. We can then continue our growth patterns (limited or expanded by resource and energy availability of course – but that’s another story for another day).

Well let’s look at where we are now and then cover the BIS report and statements, which cover its complete policy reversal.

Actual Global Sovereign Debt (solely Debt issued by our Governments in the form of Sovereign Bonds) as of 2013 is near 56 Trillion – growing nicely. Up 24% since 2011 estimated number and 311% since 2001 actual number. Completely sustainable you may say !

Actually as of Q2 2014 Global Sovereign Debt is over 58 Trillion and growing rapidily....see Mckinsey report

Well let’s look at this in more detail.

From 2001 to 2007, Sovereign Debt rose by 67% or a Yearly Compound Growth of 9%.

From 2007 to 2013, Sovereign Debt rose by 87% or a Yearly Compound Growth of 11%.

Do you see the problem here ?

The World was supposed to enter a Depression like De-leveraging event in 2008 to actually reduce our debt loads, instead due to the policy decisions by our respective Governments and Central Bankers (to keep the party going) we have actually increased the velocity of our debt increases on a yearly compound rate of growth !

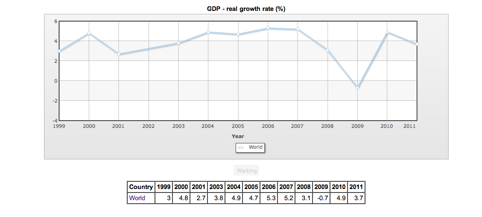

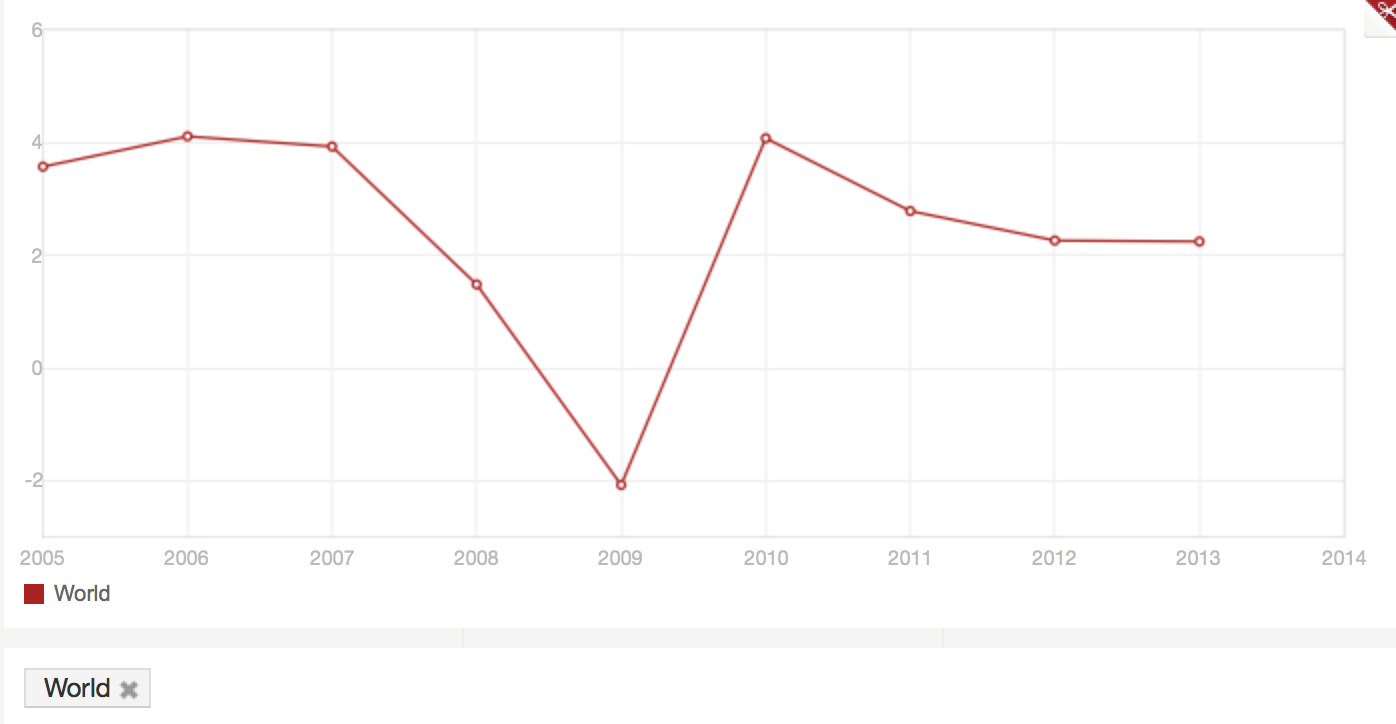

Our World GDP growth in comparison (Note: This is actually not Real GDP as a manipulated Inflation Deflator was used)

A global GDP Picture below from The World Bank

World GDP reported again at 2.2% for the full year 2013 by the World Bank.

As you can clearly see our debt growth situation against our GDP income growth (GDP – Market Value of overall output and production of good and services in a given period) is completely out of control. Rather than correct our historical debt insolvency; beginning in 2007, we have actually gone in the opposite direction due to massive manipulation by the “Powers that Be” to keep the party going.

We are now in an even larger crisis of truly unprecedented proportions than we found ourselves in 2007/8.

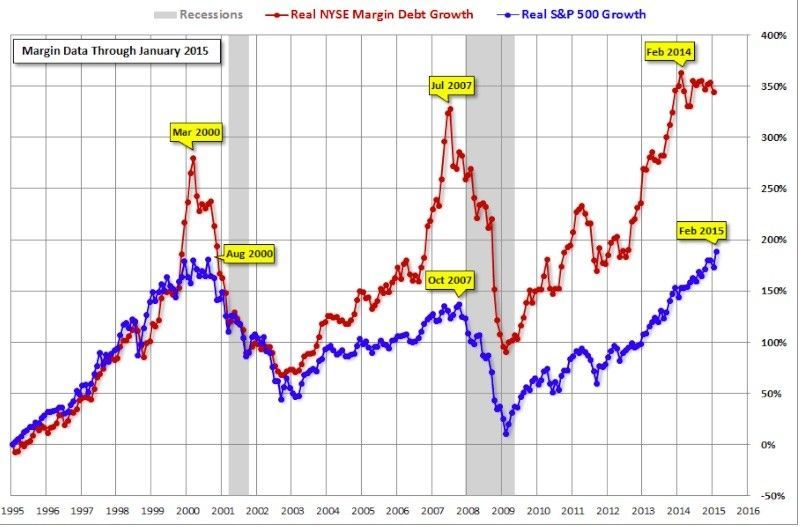

If anyone thinks we are on the road to normality and growth patterns due to the rising Stock Markets the last few years (stock market margin debt has clearly passed historical records in the stock market), or an improving housing situation (debt leverage in the UK property market for instance again at new all time record highs), then you really do not understand mother nature and simple mathematics.

Chart: Traders betting on stocks with record debt, courtesy of Business Insider

But that’s not the whole Debt Picture, it’s actually much worse…

Total World Debt hit US$ 223.3 Trillion (313% of GDP) as of the end of 2012, according to a research piece put out by ING. Debt in the developed economies amounted to US$ 157 Trillion or 376% of GDP (440 % in G7 Economies) or US$ 170,000 per man, woman and child in the developed World.

No problem there then ?

This insurmountable debt mountain will collapse at some point and bring down the World Financial System, as we know it.

Over the past five years in the developed world, it took $18 dollars of debt (of which 28% was provided by central banks) to generate $1 of growth.

Kyle Bass comments…

Trillions of dollars of debts will be restructured and millions of financially prudent savers will lose large percentages of their real purchasing power at exactly the wrong time in their lives. Again, the world will not end, but the social fabric of the profligate nations will be stretched and in some cases torn. Sadly, looking back through economic history, all too often war is the manifestation of simple economic entropy played to its logical conclusion. We believe that war is an inevitable consequence of the current global economic situation.

The Emerging economies of the World had debt to GDP of 224%, bringing the overall World Debt load down to an average of 313% and growing, but still 130 % above mathematical sustainable levels (according to the World Bank, OECD and IMF) – which requires a de-leveraging / default of near 100 Trillion US$ World wide !

This does not include China’s Shadow Banking System Debt, World Unfunded Liabilities or War costs and reparations – see a problem here ?

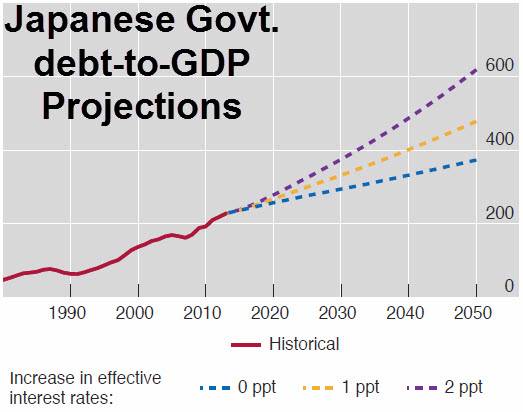

Then you have the BIS (Bank for International Settlements – The Central bank of Central Banks) issuing a chart below of Japanese debt loads based of effective interest rates they will have to pay going forward (via zerohedge).

As you can see below, mathematics simply take over !!

BIS recent announcement on complete policy reversal

BIS warns Monetary Kool-Aid part is over…

Central Banks’ Central Bank, aka the Bank of International Settlements (or BIS) in Basel where the MIT central-planning braintrust meets every few months to decide the fate of the world, warned that the Fed-induced collateral shortage is distorting the markets.

Bank for International Settlements (BIS) warns about the dangers of re-hypothecation.

They have now come to the conclusion that I and many others (obviously including the Austrian School of Economics and Zerohedge) have been re-iterating time and time again that the only conclusion to all of this is a complete collapse of our present Monetary System itself.

Rather than type myself, I will copy & paste some of their direct comments (in blue) from their report, with my conclusions at the end…

Since the beginning of the financial crisis almost six years ago, central banks and fiscal authorities have supported the global economy with unprecedented measures. Policy rates have been kept near zero in the largest advanced economies. Central bank balance sheets have doubled from $10 trillion to more than $20 trillion. And fiscal authorities almost everywhere have been piling up debt, which has risen by $23 trillion since 2007. In emerging market economies, public debt has grown more slowly than GDP; but in advanced economies, it has grown much faster, so that it now exceeds one year’s GDP.

Consider what would happen to holders of US Treasury securities (excluding the Federal Reserve) if yields were to rise by 3 percentage points across the maturity spectrum: they would lose more than $1 trillion, or almost 8% of US GDP (Graph I.3, right-hand panel). The losses for holders of debt issued by France, Italy, Japan and the United Kingdom would range from about 15 to 35% of GDP of the respective countries. Yields are not likely to jump by 300 basis points overnight; but the experience from 1994, when long-term bond yields in a number of advanced economies rose by around 200 basis points in the course of a year, shows that a big upward move can happen relatively fast.

And while sophisticated hedging strategies can protect individual investors, someone must ultimately hold the interest rate risk. Indeed, the potential loss in relation to GDP is at a record high in most advanced economies. As foreign and domestic banks would be among those experiencing the losses, interest rate increases pose risks to the stability of the financial system if not executed with great care.

* * *

Easy financial conditions can do only so much to revitalise long-term growth when balance sheets are impaired and resources are misallocated on a large scale. In many advanced economies, household debt remains very high, as does non-financial corporate debt. With households and firms focused on reducing their debt, a low price for new credit is not terribly relevant for spending. Indeed, many large corporations are using cheap bond funding to lengthen the duration of their liabilities instead of investing in new production capacity. It does not matter how attractive the authorities make it to lend and borrow – households and firms focused on balance sheet repair will not add to their debt, nor should they.

And, most of all, more stimulus cannot revive productivity growth or remove the impediments that block a worker from shifting into a promising sector. Debt-financed growth masked the downward trend in labour productivity and the large-scale distortion of resource allocation in many economies. Adding more debt will not strengthen the financial sector nor will it reallocate resources needed to return economies to the real growth that authorities and the public both want and expect.

* * *

Six years have passed since the eruption of the global financial crisis, yet robust, self-sustaining, well balanced growth still eludes the global economy. If there were an easy path to that goal, we would have found it by now. Monetary stimulus alone cannot provide the answer because the roots of the problem are not monetary. Hence, central banks must manage a return to their stabilisation role, allowing others to do the hard but essential work of adjustment.

Ultimately, outsize public debt reduces sovereign creditworthiness and erodes confidence. By putting their fiscal house in order, governments can help restore the virtuous cycle between the financial system and the real economy. And, with low levels of debt, governments will again have the capacity to respond when the next financial or economic crisis inevitably hits.

Now this is absolutely huge news, one which is completely obvious but nonetheless. The BIS who fully supported the policy response of negative real interest rates around the World and massive money printing have come to the conclusion that it just is not working!

Rather than the World using this emergency policy response to de-leverage it’s extreme debt load in an orderly fashion it has actually increased it’s debt leverage.

The BIS have come to the only possible conclusion, this will end and it will end very shortly (months to a few short years ?) in an enormous disaster for the Financial Industry and the Monetary System itself.

Remember the BIS statement above, in the USA alone a 3% move in rates would be equal to a loss of over 1 Trillion US$ on holders of this debt (banks being a big part of that).

Is a sovereign debt crisis looming ?

....

Conclusion

My conclusion on how this will ultimately play out and effect precious metals can be seen here..

Disclaimer : The information contained in this website should be used as general information only. It does not take into account the particular circumstances, investment objectives and needs for investment of any investor, or purport to be comprehensive or constitute investment advice and should not be relied upon as such. You should consult a financial adviser to help you form your own opinion of the information, and on whether the information is suitable for your individual needs and aims as an investor. You should consult appropriate professional advisers on any legal, taxation and accounting implications before making an investment.